Crypto Wallet Safety: IRS Tax Rules and Strategies

by Julian Weber

Hey, it’s Julian Weber, your Chicago-based tax advisor. Ever thought your crypto wallet—whether it’s holding Bitcoin, Ethereum, or some quirky altcoin—was your private little vault? I did too, until a chilling moment a few years back hit me like a ton of bricks. While reviewing a client’s records, I realized the IRS has its eyes on every blockchain move you make. It felt like a scene from The Wolf of Wall Street, where reckless financial excess crashes into harsh reality—only this time, it’s digital coins under the spotlight. Stick with me as I break down why your crypto wallet could land you in hot water with the IRS, share hard data from my decade as a tax consultant, and give you actionable steps to stay safe. Trust me, an IRS notice is not the Monday morning surprise you want.

A Wake-Up Call in a Chicago Blizzard

Picture this: it’s 2017, and I’m in my Chicago office, the wind howling outside during a brutal Lake Michigan blizzard. A client, let’s call him Dave, walks in looking like he’s seen a ghost. He’d turned a $5,000 Bitcoin investment into $120,000 in just six months. “Julian, it’s all online. No one knows, right?” he asked, sipping a dark roast Americano I’d brewed to ease his nerves. I had to break the news: the IRS isn’t blind. Since 2014, they’ve classified crypto as property, meaning every trade or sale is taxable. Dave nearly choked when I calculated he owed over $27,000 in capital gains tax at the 23.8% long-term rate for high earners (per IRS brackets for that year). And that’s before penalties for not reporting.

That moment stuck with me. Having navigated IRS audits myself—including a gut-wrenching one in 2012 that triggered my own panic disorder—I knew crypto tax rules were no joke. The IRS has recovered over $10 billion in unreported crypto taxes since ramping up enforcement, according to their 2022 annual report. And here’s the kicker: since 2019, Form 1040 asks right at the top, “Did you receive, sell, exchange, or dispose of any virtual currency?” Answering “no” when you’ve got activity is a red flag for an audit. With tools like Chainalysis and reports from exchanges like Coinbase, your “private” wallet isn’t so private.

The Taxable Events You Didn’t See Coming

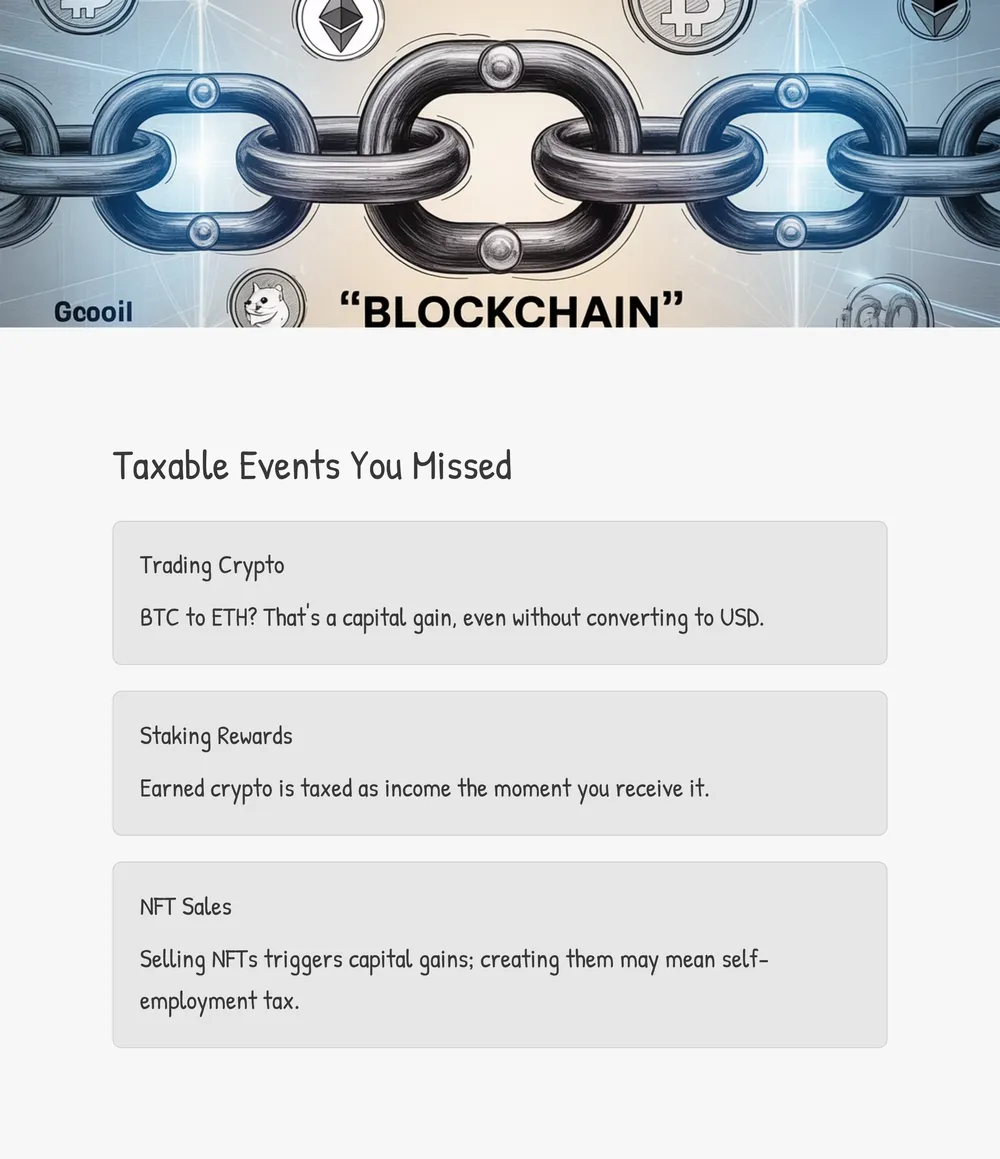

Let’s get into what the IRS considers taxable. It’s not just buying and selling. I’ve seen clients blindsided by these rules, and I don’t want you to be next. First up, capital gains tax. Every sale or trade—whether to USD or another crypto—triggers a taxable event. Bought 1 Bitcoin at $10,000 in 2020 and traded it for Ethereum at $50,000 in 2021? That’s a $40,000 gain, taxed at short-term rates (up to 37%) or long-term rates (0–20% plus 3.8% Net Investment Income Tax) based on holding time and income. IRS data shows over 8.7 million Americans reported crypto transactions in 2022, but millions more likely didn’t, often unaware trades count.

Then there’s staking or mining income. Earn rewards from staking Ethereum or mining Bitcoin? It’s taxed as ordinary income the moment you get it. If you earned 0.1 ETH worth $300, that’s $300 added to your taxable income, even if you don’t sell. Last year, a client earned $12,000 in staking rewards via Lido Finance but didn’t report it, thinking it wasn’t “real money.” The IRS hit him with a $3,000 bill plus a 5% penalty. And don’t forget NFTs—selling one for profit is a capital gain, while creating and selling your own could mean self-employment tax at 15.3%. A 2023 New York case saw an NFT artist owe $45,000 after selling art for $200,000. These aren’t just hypotheticals; they’re real risks.

Form 1040: The IRS Trap You Can’t Ignore

That Form 1040 question isn’t just a checkbox—it’s a declaration under penalty of perjury. Answer “no” but get caught with unreported crypto, and the IRS can claim willful evasion, hiking penalties from 5–25% for negligence to 75% for fraud. In 2021, they sent over 10,000 “soft letters” warning suspected crypto holders to amend returns or face audits. I’ve helped clients through this, and the stress is real—imagine explaining a $50,000 penalty notice to your spouse over deep-dish pizza at Lou Malnati’s on a Friday night. Checking “yes” might invite scrutiny, but checking “no” falsely is a bigger gamble. As someone who’s biked along Lake Shore Drive worrying about a client’s audit, I’m telling you: don’t roll the dice.

My Own Crypto Tax Scare

I’ll be real—crypto taxes tripped me up too. In 2018, after burgers with my CPA buddy Marcus Chen at Portillo’s, I bought $2,000 of Ethereum as an experiment. I swapped half for Chainlink during a spike, netting a $1,500 gain. Come tax season, I nearly forgot to report it. If I hadn’t caught it on TurboTax, I could’ve faced a $300 penalty for underreporting. It was a wake-up call. Now, I track every move and urge my clients to do the same. It reminds me of Black Mirror’s “Nosedive,” where every action is tracked. The blockchain is like that—every transaction recorded, with the IRS watching. You don’t want to end up like Dave with a huge bill or dodge a bullet like I did. Get ahead of it.

Protect Your Crypto Wallet: Actionable Tips

How do you keep your crypto wallet from becoming an IRS target? I’ve distilled a decade of tax advisory experience into simple steps you can start today. These are the same tips I share with clients over coffee runs to Starbucks on Michigan Avenue.

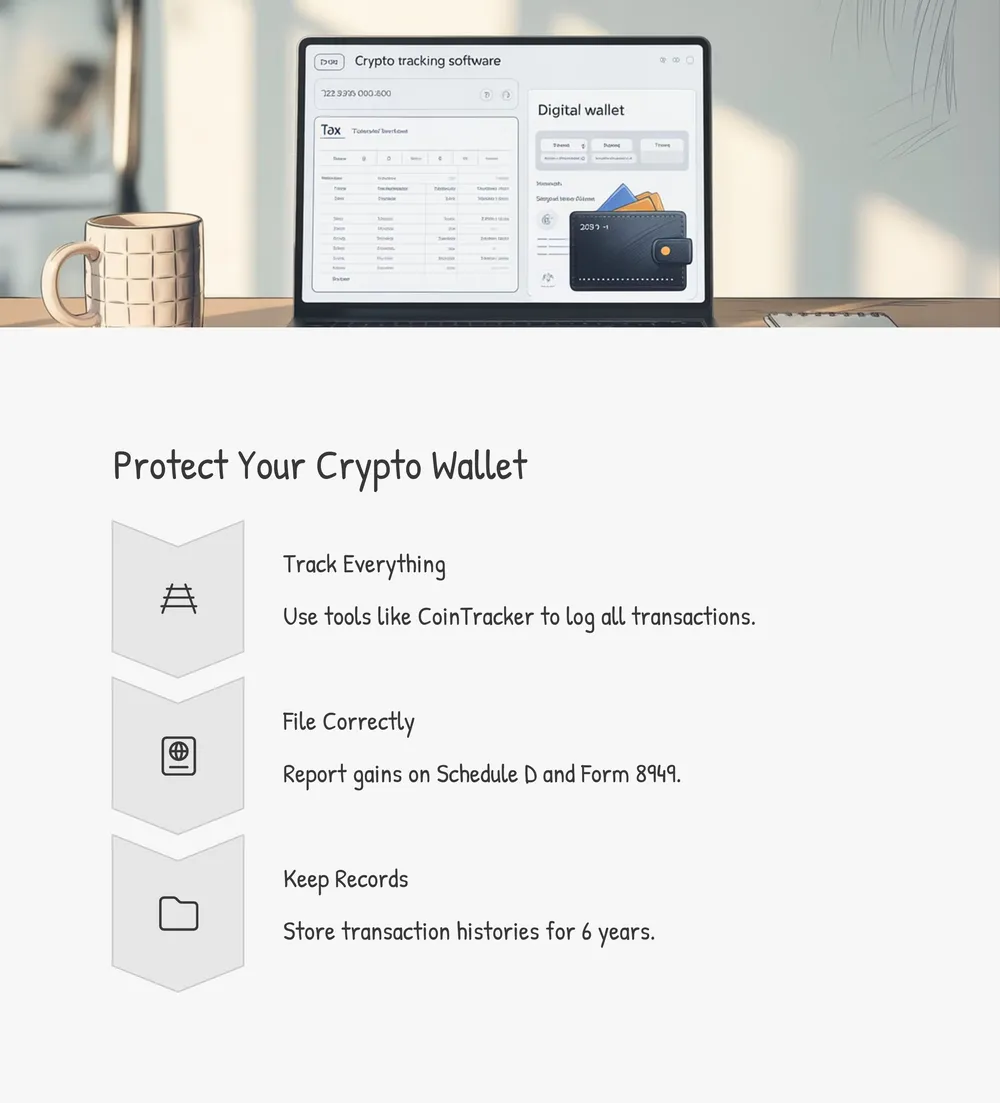

- Track Every Transaction: Use a tool like CoinTracker ($59/year at cointracker.io) to log buys, sells, and rewards. Sync wallets via API keys in “Wallet Connections”—takes just 10 minutes.

- Answer Form 1040 Honestly: Check “yes” if you’ve had any crypto activity, even just holding. It’s safer than risking an audit.

- File the Right Forms: Report gains on Schedule D and Form 8949; staking income on Schedule 1. Download them at irs.gov.

- Keep Records for 6 Years: The IRS can audit up to 6 years back. Store transaction histories securely on Google Drive with 2FA enabled.

- Watch Airdrops and Forks: Free crypto is taxable as income. Check wallet history on Etherscan.io for unexpected deposits.

- Consult a Pro: If your portfolio tops $50,000 or involves DeFi, hire a crypto tax specialist. Costs start at $500 in Chicago—cheaper than a $10,000 penalty.

Why Compliance Is Your Safety Net

Beyond dodging penalties, reporting crypto builds a safety net. The IRS isn’t just after whales; they’ve audited small traders with as little as $10,000 in unreported gains, per a 2023 Treasury report. Non-compliance can also hurt your credit if penalties lead to liens. I’ve seen clients miss mortgages over unresolved tax debts—it’s not just money, it’s your future. Plus, with the 2021 Infrastructure Act tightening broker reporting starting in 2024, more data will flow to the IRS. Staying ahead isn’t just smart; it’s survival. In my next post, I’ll dive into IRS Notice 2014-21, decode transaction types like airdrops, and review tools like CoinTracker and Koinly after hours untangling my own trades.

Quick Crypto Tax Reference

| Transaction Type | Taxable Event? | Tax Type | Reporting Form | Example Value |

|---|---|---|---|---|

| Buying Crypto with USD | No | N/A | N/A | $5,000 BTC purchase |

| Selling Crypto for USD | Yes | Capital Gain/Loss | Schedule D, Form 8949 | $10,000 gain on BTC sale |

| Trading Crypto for Crypto | Yes | Capital Gain/Loss | Schedule D, Form 8949 | $2,000 gain BTC to ETH |

| Staking/Mining Rewards | Yes | Ordinary Income | Schedule 1 | $500 ETH staking reward |

| NFT Sale (Profit) | Yes | Capital Gain | Schedule D, Form 8949 | $1,500 NFT profit |

Frequently Asked Questions

Do I have to report crypto if I didn’t sell anything?

Yes, if you received crypto via staking, mining, or airdrops, it’s taxable as income even if you hold it. Only buying and holding with no transactions isn’t reportable, but you still answer “yes” on Form 1040 if you own crypto.

What if I use a decentralized wallet the IRS can’t track?

Don’t bet on anonymity. The IRS uses blockchain analytics like Chainalysis to trace transactions, even on decentralized wallets. Exchanges often report data too, linking your identity to addresses.

How much are the penalties for not reporting crypto?

Penalties start at 5% of unpaid tax for negligence, escalating to 25% for substantial underpayment, and up to 75% for fraud. Late filing adds 5% per month up to 25%, per IRS rules.

Can I deduct crypto losses to offset gains?

Yes, capital losses can offset gains, and if losses exceed gains, you can deduct up to $3,000 annually against other income on Schedule D. I’ve helped clients save thousands this way.

Take Control Before It’s Too Late

Navigating crypto taxes feels like driving my Volvo XC90 through a Chicago snowstorm—daunting, but doable with the right prep. I’ve seen the fallout of ignoring these rules, from Dave’s $27,000 bill to my own near-miss with a small Ethereum trade. With over 50% of Americans owning digital assets per a 2023 Statista survey, IRS enforcement will only tighten. So, take a sec this week—are you tracking every trade? Ready to answer Form 1040 honestly? Start small: download CoinTracker or grab your exchange statements today. And don’t miss my next post, where I’ll decode IRS crypto reporting and review tax software to simplify compliance. Got a crypto tax question? Drop it below—I’m all ears!

※ This article is for informational purposes only and does not constitute professional advice.